Understanding Blockchain: Everything you need to know

Hunter Johnson

Posted on May 30, 2023

This article was written by Mohsin Abbas, a member of Educative's technical content team.

As technology continuously evolves, blockchain has undeniably captured the interest of individuals and companies all around the globe. This incredible invention is altering numerous sectors, generating new possibilities and ways of working that revolutionize how we handle data and transactions.

This comprehensive blog will explain blockchain technology by diving deep into its beginnings, main components, uses, and benefits. It will explore how this digital transformation enhances transparency, security, and openness for a better future and cover its potential to disrupt traditional systems and create innovative solutions. It will also explain how various industries embrace blockchain technology to overcome challenges, improve efficiency, and foster stakeholder trust.

The story of blockchain

To acquire a thorough grasp of the blockchain story, a good start is to investigate its beginnings. This revolutionary technology was initially developed in 2008 by a person or group using the name Satoshi Nakamoto, as described in the white paper “Bitcoin: A Peer-to-Peer Electronic Cash System.”

Since Satoshi Nakamoto’s true identity is still unknown, the origins of blockchain technology are mysterious. Nevertheless, it is generally agreed that Satoshi wanted to create a decentralized, ungoverned digital monetary system.

On January 12, 2009, Satoshi Nakamoto sent 10 bitcoins to computer programmer and early adopter Hal Finney, officially starting the Bitcoin network. Originally, blockchain was intended to serve as Bitcoin's underlying infrastructure. But, its potential has now been recognized outside the area of cryptocurrency, creating a more trustworthy, transparent, and secure alternative to old systems. Blockchain technology has applications in many businesses and situations beyond its initial intent. As its adoption spreads, we continue to uncover new ways to leverage it to solve complex problems, streamline operations, and reshape industries in the modern era.

The internal workings of the blockchain

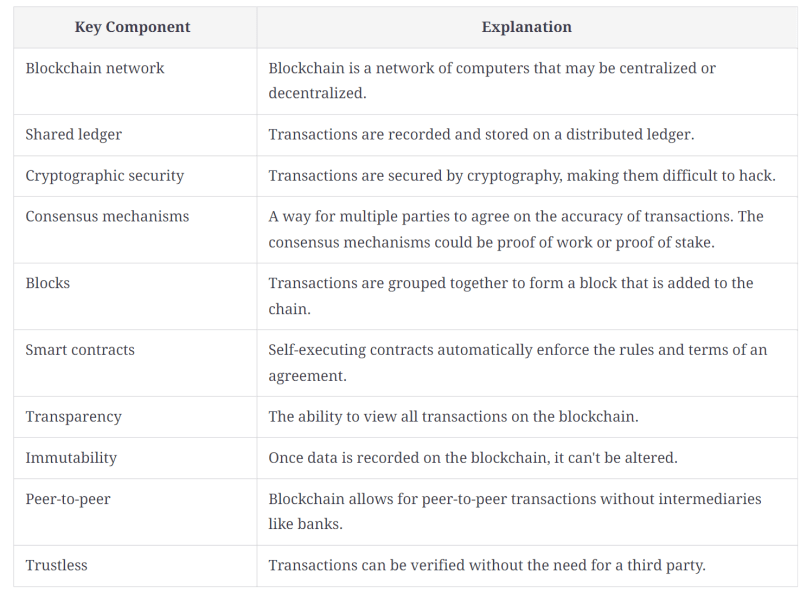

Now that the history has been explored, understanding blockchain's inner workings is the next task. A number of essential elements give blockchain technology its power. Added below is a table that can help explain blockchain's key components.

Components of a Blockchain:

How does the blockchain system work?

These elements (the key components) serve as the framework for the whole blockchain ecosystem. Knowing how they interact together is the key to understanding blockchain's internal workings.

There are two types of blockchain networks—centralized and decentralized. Decentralized blockchains share authority and decision-making among numerous nodes. On the other hand, centralized blockchains are managed by a single body, providing better efficiency and scalability but at the expense of higher centralization as well as potential attack and corruption concerns. Generally, decentralized blockchains are preferable for many applications since their benefits typically surpass those of centralized ones.

Every participating node has access to a copy of the shared ledger and is treated equally in terms of rights and obligations. All network transactions are publicly recorded in this shared ledger. Every transaction is recorded on the ledger, which is protected by cryptographic methods, guaranteeing the data's security and immutability.

Consensus mechanisms ensure agreement among participants about the current state of the shared ledger. To employ techniques like proof of work or proof of stake, multiple parties must agree on the accuracy of transactions. And once verified, these transactions are grouped into blocks and added to the blockchain. These blocks are then linked together, forming a secure chain.

Smart contracts, a cutting-edge feature of blockchain technology, are self-executing agreements that automatically enforce rules and obligations. They are designed to release funds, property, or data only when specific conditions are met.

Transparency in transactions is possible thanks to the open nature of the blockchain. The blockchain allows everyone to observe the complete history of transactions. The blockchain's immutability guarantees that it can't be changed once data is recorded.

Many of these characteristics of blockchain technology enable peer-to-peer trades devoid of middlemen like banks. Transactions are considered trustworthy when they can be confirmed without relying on a third party. This has the potential to completely alter numerous sectors and the way we conduct business.

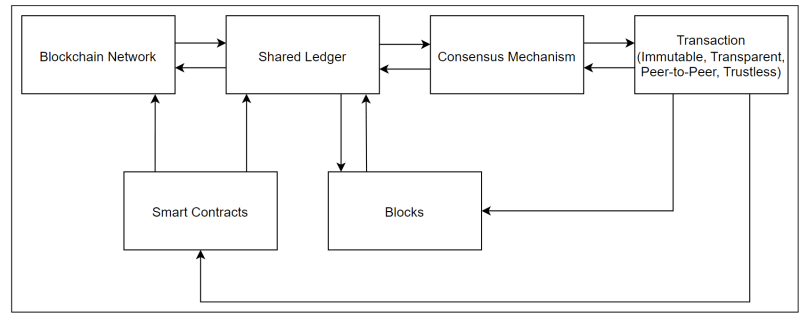

Here's an explanation of the block diagram representing the key components of a blockchain ecosystem and their interactions:

-

Blockchain Network:

- Consists of multiple participating nodes with equal rights and obligations.

- Nodes (individual computers or devices that are connected to the network) maintain copies of the shared ledger and contribute to its updates, hence the bi-directional arrow between Blockchain Network and Shared Ledger.

-

Shared Ledger:

- Serves as the public record of all transactions in the blockchain.

- Composed of a chain of blocks with a bidirectional arrow between Shared Ledger and Blocks.

- Relies on the Consensus Mechanism to maintain a consistent and agreed-upon state, represented by the bidirectional arrow between Shared Ledger and Consensus Mechanism.

-

Consensus Mechanism:

- Ensures agreement on the shared ledger's current state among participating nodes.

- Verifies and validates new transactions, represented by the bidirectional arrow between Consensus Mechanism and Transaction.

-

Transaction:

- Represents immutable, peer-to-peer, and transparent transfer of value or information within the network.

- Can initiate or interact with Smart Contracts, as shown by the arrow pointing from Transaction to Smart Contracts.

- Once verified by the consensus mechanism, transactions are grouped into blocks, as shown by the arrow pointing from Transaction to Blocks.

-

Smart Contracts:

- Enforce rules and obligations automatically through self-executing contracts.

- It can be initiated by transactions, represented by the arrow pointing from Transaction to Smart Contracts.

- Executed by nodes in the Blockchain Network, represented by the arrow pointing from Smart Contracts to Blockchain Network.

- Interact with the Shared Ledger to read or write data, represented by the arrow pointing from Smart Contracts to Shared Ledger.

-

Blocks:

- Contain a collection of verified transactions.

- Form the basis of the shared ledger, with a bi-directional arrow between Blocks and Shared Ledger.

Applications of blockchain

Cryptocurrencies, the most popular application of blockchain, are digital or virtual currencies that operate independently of a central bank or financial institution. Distinguishing between blockchain and cryptocurrencies can be difficult, but it's crucial to realize the difference in order to understand blockchain. The technology behind cryptocurrencies is called blockchain. Cryptocurrencies, which are digital or virtual currencies, utilize cryptography to secure and verify transactions as well as to control the creation of new units. Meanwhile, blockchain technology serves as the underlying foundation that enables the operation of cryptocurrencies.

Beyond cryptocurrencies, blockchain technology has a wide range of potential applications in various other industries. Here are some examples of how blockchain can be used to solve complex problems and improve processes:

Supply chain management: Streamlining supply chain management offers comprehensive transparency and visibility, which may reduce waste, mistakes, and fraud while boosting stakeholder confidence since the blockchain is safe and irreversible.

Energy trading: Peer-to-peer energy trading may use a decentralized grid, making it easier and faster for people to buy and sell energy directly with each other without middlemen. This process gives everyone more control, supports eco-friendly energy use, and helps make energy more affordable for everyone involved.

Insurance claims: By safely documenting and confirming insurance claims on the blockchain, it may be possible to lower the risk of false claims, speed up procedures, and raise customer satisfaction by building more trust and transparency.

Proof of ownership: Decentralized ownership records on the blockchain that may be used to secure digital copyright and intellectual property give visible and unchangeable proof of ownership, offer safe and effective licensing and distribution alternatives, and enable greater protection for creators.

Emission tracking: Using blockchain technology to provide safe and transparent tracking of carbon emissions and other environmental data encourages sustainability, responsibility, and openness in company practices, enabling more effective climate action.

Fundraising: Blockchain technology may offer a decentralized, open, and transparent platform for fundraising, allowing more access to funds, resources, and assistance. This technology can be used to facilitate safe and effective crowdfunding campaigns for start-ups and entrepreneurs.

Academic records: Using blockchain technology, a decentralized, transparent, and tamper-proof method for storing and verifying academic accomplishments is to create safe, unchangeable records for academic certificates and degrees. This may promote lifelong learning, skill validation, and professional advancement.

Land ownership records: The integrity of land ownership records is ensured, and fraud may be prevented by employing blockchain technology to provide safe and transparent tracking of land-ownership data.

Cultural objects: Blockchain technology may facilitate the development of decentralized platforms for the sharing and monetization of cultural objects, allowing creators and collectors to own and manage their holdings while fostering authenticity and transparency.

Healthcare: Healthcare fraud and errors can be reduced while promoting safe and transparent information sharing between patients and healthcare providers by securely storing and verifying patient data on the blockchain.

Voting systems: With the help of secure and impermeable blockchain technology, voting systems may be developed that ensure transparency and accuracy in the democratic process while guarding against manipulation, fraud, and data breaches.

Expensive goods: Blockchain technology may make it possible to authenticate expensive goods and valuable commodities in a way that is impenetrable to tampering, safeguards intellectual property rights, and prevents counterfeiting.

Advantages of blockchain technology

The following are some of the advantages of blockchain technology:

Security: The data held in blockchain technology is protected using cryptographic methods, making it nearly impossible for hackers to penetrate.

Transparency: The public ledger used by blockchain technology creates a transparent platform for all transactions. As a result, trust and accountability are ensured since all participants can see and confirm the transaction information.

Immutability: The records on the blockchain cannot be altered, moved, or changed easily.

Scalability: Blockchain technology can be tailored for applications that require fast processing since certain blockchain implementations can handle many transactions per second.

Efficiency: As blockchain technology removes middlemen from transactions, it takes less time and money to conduct a transaction. Processes may be greatly streamlined and efficiency may be increased in a variety of sectors as a result.

Adaptability: Because of its flexibility and wide-ranging applications, blockchain technology is now a popular choice for developing innovative business models and finding solutions to complex problems.

Conclusion

It's essential to understand blockchain technology since it has the ability to transform industries and how transactions are conducted. It offers a more secure, open, and transparent alternative to conventional systems that can boost productivity and cut costs for businesses. People and corporations can decide whether to use blockchain in their operations by thoroughly knowing how it operates and its potential applications.

Although blockchain has far-reaching potential beyond its current applications, understanding its underlying workings can help people remain ahead of the curve and identify fresh chances for innovation. It's crucial to have a rudimentary understanding of blockchain technology as it continues to advance and gain recognition if one is to stay up to date in the quickly evolving field of modern technology.

Your next learning steps

For advanced blockchain knowledge, take a look through the selection of specialized courses on the Educative platform listed below to deepen your understanding and expertise on the subject of blockchain. These courses address a range of blockchain-related subjects, from the fundamentals to more complex ideas. You can learn more about blockchain and its uses, as well as acquire useful skills that will benefit your career.

Some outstanding blockchain courses from Educative include the following:

Don't pass up this chance to increase your blockchain knowledge and expertise. Take the first step toward becoming a blockchain expert and enroll in Educative courses!

Posted on May 30, 2023

Join Our Newsletter. No Spam, Only the good stuff.

Sign up to receive the latest update from our blog.

Related